Eyeing an M&A Rebound

-

Minute Read

-

Listen

Stop

Stop

-

Text Bigger | Text Smaller

As the Coronavirus pandemic spread globally and financial markets were impacted, we saw unprecedented disruption in M&A activity, and the Food, Consumer and Retail space was no exception, but as we look to the second half of 2020, deal-making may return faster than expected.

Shelter-in-place restrictions saw most businesses shelve growth plans, and focus on their balance sheets and conservation of capital. As companies faced disruptions across their business activities, from supply-chain and sourcing to office shutdowns, valuations fell and both buyers and sellers became reluctant to execute on growth or exit strategies. With concerns about accessing capital markets, we saw increases in draw-downs on revolvers.

This was especially clear during the week of April 17, when there were no deals announced were over $1 billion, something not seen in over more than 15 years.

To be sure, until there is more clarity around the severity and length of the COVID impact, it will be difficult to envision large, transformative M&A transactions.

Some transactions are still being completed, especially between companies in the same sector and in already-advanced discussions. Among recent transactions that we advised on were CD&R’s acquisition of Radio Systems, announced in May, and Rise Baking Company’s agreement in March to acquire the North American frozen manufacturing business of Dawn Foods.

New Environment

We are clearly in a new and evolving environment for deal-making.

Operational uncertainty means buyers are refocusing due diligence of targets to take a harder look at supply-chain risks and exposure to customers in highly infected buyers’ regions. Sellers will need to be more flexible on purchase price adjustment mechanisms, given the potential for deterioration in the business.

With offices and factories in lockdown and amid significant travel restrictions, due diligence is hampered by the difficulty of conducting in-person management presentations, although that’s been partially offset by virtual meetings and video conferencing.

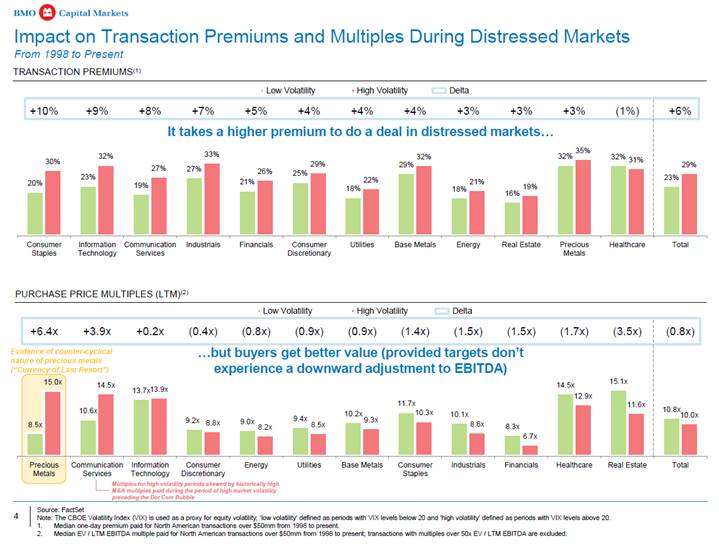

Valuations are challenging. While deals are typically valued based on multiples of revenue or EBITDA, in a COVID-19 world, sellers of public companies will seek higher purchase-price premiums and argue that the fundamentals of their business have not changed.

Figure – comparison of purchase price premiums during periods of distressed markets or high volatility to regular markets.

In the FCR space, history has shown that consumer staples show the highest delta – oftentimes achieving the highest premiums – during distressed markets.

Stock-for Stock Deals

Trends that are developing include an increase in equity as a percentage of purchase prices, and we expect an uptick in all-stock transactions in 2020 to drive public-to-public, and public-to-private M&A.

In the near term, we expect a further increase in buyers’ use of protection clauses that afford them the option of walking away from M&A agreements if conditions materially worsen. We are already seeing examples of this, like the Sycamore/Victoria’s Secret deal that was recently terminated without either party paying a fee to the other side.

In FCR, we are seeing a fairly wide variance in trends emerge across sub-sectors, depending on the discretionary/non-discretionary nature of the business. The food distribution and food retail subsectors have remained resilient, despite an overall negative downturn across the sector.

Reasons for Optimism

While an M&A rebound tends to normally lag recovery from an economic crisis by two to four quarters, there are reasons we could see deal-making recover more quickly than in previous downturns, and rebound more in line with equity and debt markets.

With record levels of dry powder, we expect sponsors to lead the market upward as they take advantage of low valuations, leading to an uptick in take-private activity; sponsors will likely focus efforts on their portfolio companies and add-ons as a first priority.

In contrast with the last economic crisis, when Private Equity was poorly capitalized and credit markets were frozen, sponsors are much stronger this time around. From our active discussions with PE clients, we know their appetite to acquire is high, given ample supply of unspent equity, and, as debt markets continue to return to normal, we expect them to be more active.

As the economic downturn continues, so too will the frequency of distressed situations, creating opportunities for well-positioned activists and hedge funds to increase ownership in companies they already own, and look to influence business decisions.

Market dislocation will drive an uptick in public M&A from well-capitalized buyers, and we anticipate an increase in unsolicited and hostile activity.

Defense Versus Offense

Similar to the 2008 crisis and the preceding tech bubble, there’s already been a dramatic increase in shareholder rights plans, known as poison pills, and we recommend that corporations prepare themselves as they think about their own strategic alternatives, from a defensive as well as an offensive perspective.

When activism is on the rise, corporations should be engaging with their shareholders, and revisiting shareholder rights plans would also be prudent. Balance sheets should be analyzed for optimal capital structure, and companies struggling with liquidity concerns should be open-minded to conversations around strategic investments.

Companies that have the benefit of liquidity should preserve it, but remain vigilant for the right moment to make add-on acquisitions.

We are going through difficult times, but for many businesses, the fundamentals have not changed and there are good values to be had. Businesses should continue to evaluate ongoing options and assess opportunities. Now may be a good time to revisit discussions that were had in the past as some sellers face liquidity constraints and are more open to an approach.

As consumers gradually shift to more normal purchase behaviour, sellers will have greater conviction when estimating their future performance, and buyers will be more inclined to bid for the future with this added credibility.

For more information contact lyle.wilpon@bmo.com

Additional materials on M&A from the BMO Farm to Market conference:

Road to Recovery 2020

PART 1

America’s Post-Pandemic Economic Prospects

Michael Gregory, CFA June 29, 2020

After dealing with the steepest, deepest, and fastest recession in history, there are clear indications that the U.S. economy has be…

PART 3

Food Supply Chain: Lessons Learned from COVID-19

Michael Johns July 27, 2020

The COVID-19 pandemic put significant stress on the food supply chain. From manufacturers to distributors to retailers, all links in the ch…

PART 4

Optimizing Liquidity in an Uncertain Environment

None August 10, 2020

While COVID-19 has put pressure on businesses of all sizes in 2020, the Corporate Treasurer has been dealing with some level of uncertainty…

PART 5

COVID-19 Underscores the Evolution in Electronic Trading

Aine O’Flynn August 24, 2020

There is no turnkey response to the COVID-19 pandemic that has left no facet of life unscathed, as nations, governments, industries and soc…

PART 6

Did COVID Actually Save Retail?

Simeon Siegel, CFA September 18, 2020

As retailers choose which stores to open, rather than close, on the heels of the COVID-19 outbreak, they face a once-in-a-lifetime opportun…

PART 7

Road to Recovery: Pandemic in Perspective

Dan Barclay, Brian Belski, None October 02, 2020

With North America six months into the fight against COVID-19, and as the world contemplates a potential second wave of the pandemic, some …

PART 8

Spectacular SPACs – The Unicorns Are Coming

Eric Benedict October 28, 2020

They’ve been called a flash in the pan by market pundits, critiqued for questionable returns, but the so-called Special Purpose Acqui…