Driving Sustainable Outcomes: Canada’s First Labelled Green Loan

Driving Sustainable Outcomes: Canada’s First Labelled Green Loan

Head, Sustainable Finance, Products and Strategy

John Uhren is Managing Director and Head, Sustainable Finance, Products and Strategy, at BMO. He leads product development and strategic initiatives across the ente…

John Uhren is Managing Director and Head, Sustainable Finance, Products and Strategy, at BMO. He leads product development and strategic initiatives across the ente…

VIEW FULL PROFILE-

Minute Read

-

Listen

Stop

Stop

-

Text Bigger | Text Smaller

Labelled Green Loans have come to Canada, adding an important new tool to companies wishing to finance a wide range of projects that provide clear environmental benefits.

BMO’s Commercial Banking, Capital Markets and Sustainable Finance teams recently helped deliver the first labelled Green Loan in Canadian history. The labelled Green Loan was provided to Atlantic Packaging, with loan proceeds used to finance a new 100% recycled containerboard facility in Whitby, Ontario. In conjunction with the loan, BMO worked with Atlantic to publish a Green Financing Framework containing additional information on the loan and the company’s overarching commitment to a sustainable future.

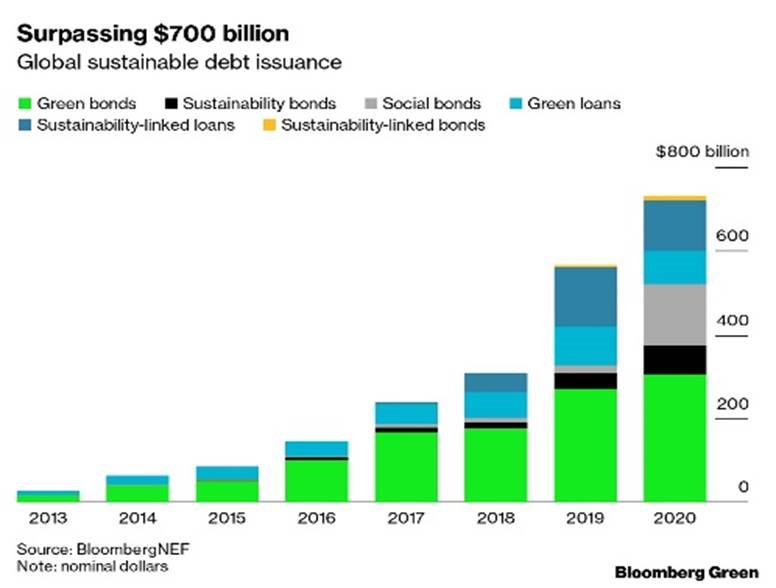

The Green Loan category is still nascent, making up approximately US$80bn of US$700bn in sustainable debt issued globally in 2020, with Green Bonds, Social Bonds and Sustainability Linked Loans making up the lion’s share of issuance.

SOURCE: BloombergNEF

By structuring the first labelled Green Loan in Canadian history, BMO is once again at the forefront of delivering innovative products to our clients, and in turn driving a sustainable future for all.

In December 2019, BMO Capital Markets entered into an agreement to provide Maple Leaf Foods with the first sustainability-linked loan in Canada.

What is a Labelled Green Loan?

Labelled Green Loans are any type of loan instrument that aligns with the Green Loan Principles (GLPs). The GLPs were published in 2018 by the Loan Market Association, Asia Pacific Loan Market Association, and Loan Syndications and Trading Association to promote the development and integrity of the green loan market.

The Four Core Components of the GLPs Are:

-

Use of Proceeds – the green loan proceeds must be used for green projects that provide clear environmental benefits. The GLPs provide non-exhaustive categories of eligibility, including renewable energy, clean transportation, eco-efficient adapted products, and more.

-

Process for Project Evaluation and Selection – the borrower should clearly communicate its environmental sustainability objectives and the process by which it selects green projects for financing.

-

Management of Proceeds – the proceeds of a green loan should be tracked by the borrower to maintain transparency.

-

Reporting – the borrower is encouraged to keep readily available information on the use of proceeds and the expected impact.