After the Bank Failures, 6 Questions to Help CFOs Diversify Deposits

After the Bank Failures, 6 Questions to Help CFOs Diversify Deposits

Head of Coverage, Industries, and Structured Finance, Bank of the West

Work Experience: Bank of the West - EVP, Head of Coverage, Industries and Structured Finance, Commercial Banking Group (“CIS”) Key Accomplishments &a…

Work Experience: Bank of the West - EVP, Head of Coverage, Industries and Structured Finance, Commercial Banking Group (“CIS”) Key Accomplishments &a…

VIEW FULL PROFILE-

Minute Read

-

Listen

Stop

Stop

-

Text Bigger | Text Smaller

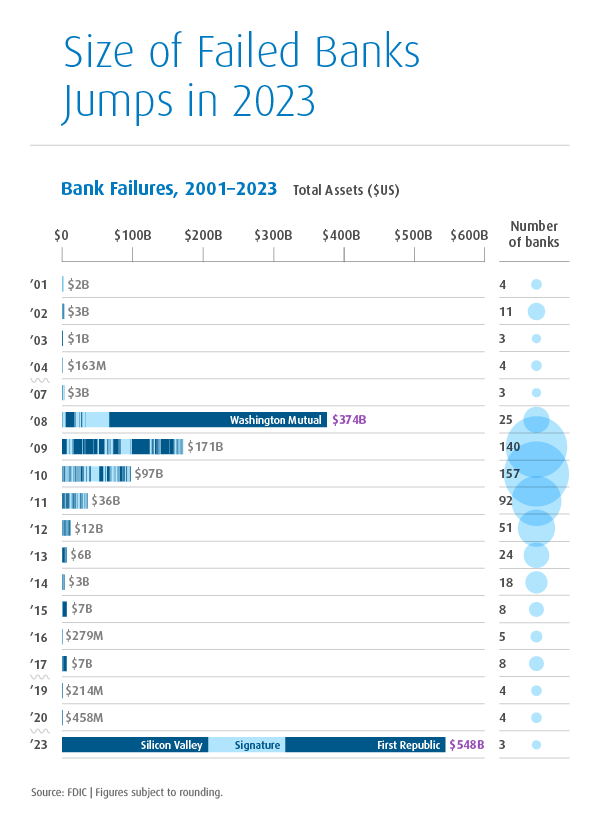

The US has a long history of bank failures1, but this year is exceptional. So far in 2023, regional lenders with assets of nearly $550 billion have gone under, exceeding the size of the banks toppled in 2008 at the height of the financial crisis.

Higher borrowing costs and the prospect of a US recession were risks even before regulators shuttered Silicon Valley Bank. So far, the economic impact of the bank failures has been muted, but corporate finance leaders will want to make sure they understand counterparty risk and proactively manage it.

Nobel prize laureate, Harry Markowitz, once said: "Diversification is the only free lunch in finance," referring to the way in which spreading investment across asset classes or sectors can reduce portfolio risk. For some CFOs and treasurers, a diversification strategy can be applied to their corporate deposits, too. The aim is to reduce exposure to unstable financial institutions.

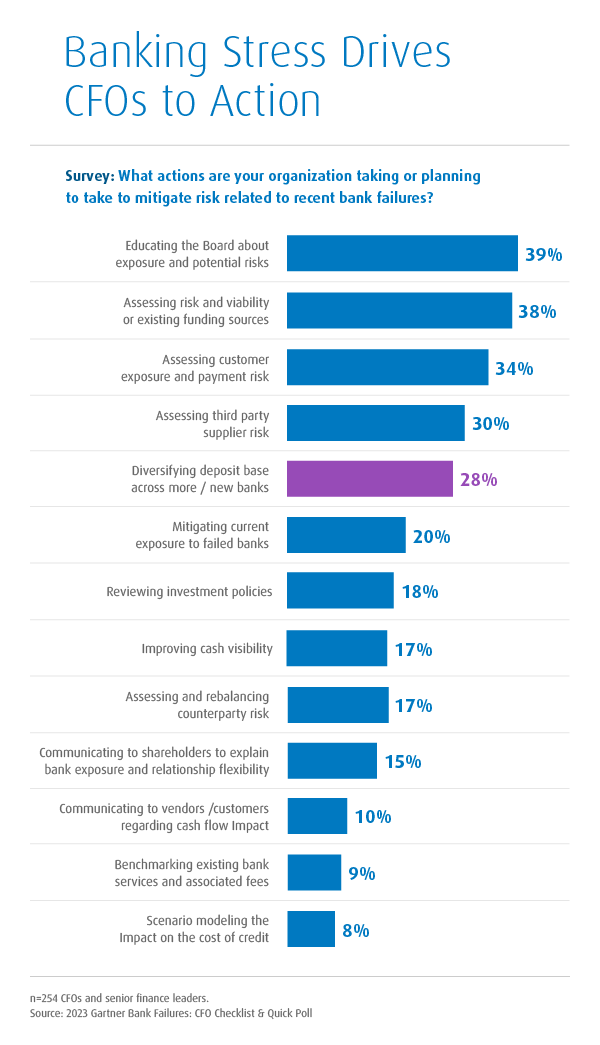

More than a quarter of CFOs planning to diversify deposits

I've seen this concept referred to as bank redundancy. But I prefer the term "deposit diversification" because the point is to manage risk rather than create more banking relationships than a company really needs.

Some finance leaders have already started planning. In a Gartner survey2, 28 percent of CFOs said they plan to diversify their deposits across more banks after recent bank failures. The survey took place in March, before regulators seized control of First Republic Bank, making it the second-largest US bank failure. The share of CFOs today planning to diversify banks could be higher.

Six questions to guide a deposit diversification strategy

To be clear, if you believe your banking partners are well-capitalized and continue to have access to adequate liquidity, then you shouldn't worry about implementing a deposit diversification strategy. You may want to consider forming a backup bank plan as a contingency (see below), but otherwise, you're good.

If you believe your organization would benefit from spreading deposits to different banks, these six questions can help inform your strategy.

1. Have you mapped out your company's cash needs and underlying risks?

A good place to start is to understand your company's cash payables and receivables. When and how much does your company need to draw from its bank accounts for operations, e.g., meeting payroll, making supplier payments, paying rent, etc.? Keep in mind any third-party payment arrangements tied to banks, too.

On the flip side, do you have full visibility on your company's income streams, including collection times and availability of funds?

It may require more time and resources to shift accounts tied to business-critical recurring payments. So, you'll want to have a clear understanding of how much cash is used to support operations, where the cash is held, and what are the underlying risks of the institutions where those accounts are.

2. Does your company have liquid reserves?

Once you've mapped out your company's cash needs, you'll be better positioned to identify cash reserves that you can spread across different institutions. It's less challenging to move these kinds of liquid funds to new bank accounts, particularly if you're tracking days payable outstanding. However, how much to put in reserve is a more difficult question.

There is a rule of thumb about keeping cash in reserve worth six months of operating expenses, but the reality is more complicated. Seasonality, industry, suppliers, cash flow forecasts, and sales pipeline can all have an impact on calculating cash reserves.

Many corporate banks have consultants who can help you map your cash flow and also take advantage of opportunities to get the most return on your reserves. Be sure to take advantage of them.

3. Have you identified other banks your company could use?

See if you can come up with a shortlist. For some, bank size may be an important factor because of the perceived stability of larger balance sheets. But make sure your company receives the level of service and attention you need. After all, corporate banking is based on relationships with customers. Your company should be receiving the right service from a provider with deep industry-specific expertise that really knows your business, and forming strong relationships no matter how many banks it uses.

In addition to level of service, other considerations are being able to access funds when your company needs them and being able to integrate new accounts with your company's financial platforms.

4. Have you considered other opportunities resulting from deposit diversification, too?

Spreading your company's cash across more banks is ultimately about risk mitigation. However, keep in mind other potential benefits. Better online portal experience, stronger geographic alignment with your company's footprint, new corporate customer incentives, capital markets coverage of the whole balance, research capabilities, and even brand affinities are all potential opportunities that may help justify the time and resources necessary to implement a diversification strategy.

5. Have you created bank report cards?

Once you've identified the banks your company is considering as part of its diversification plan, you'll want to form report cards for each candidate. In some ways, this is the reverse of what happens when a company approaches a bank for a loan and the bank conducts due diligence. Now, finance teams will look at the strength and stability of potential banking partners.

What are the potential partners' capital strength and liquidity positions relative to regulatory requirements? Do they exceed them? What's their dividend record, and have they provided strong shareholder returns? The top leadership at your company should be aware of and involved in this part of the strategy.

6. Do you have a banking backup plan?

The sudden and unexpected bank failures this year are a timely reminder that business continuity plans should include cash and liquidity provisions in case of disruption and steps to take if a primary or syndicate bank fails. Having a banking backup plan is a good idea for any finance team.

These six questions should help finance departments be better prepared for regional banking stress that has been disruptive to business and unsettling for people. But with a diversification strategy, finance leaders who see counterparty risk can take action to reduce exposure. Bank of the West joined BMO in February, and you can find more information about its financial performance. Add it to your report card.

1 FDIC: Bank Failures in Brief

2 Gartner Survey Shows 28% of CFOs Plan to Diversify Deposits Across More Banks After Recent Failures